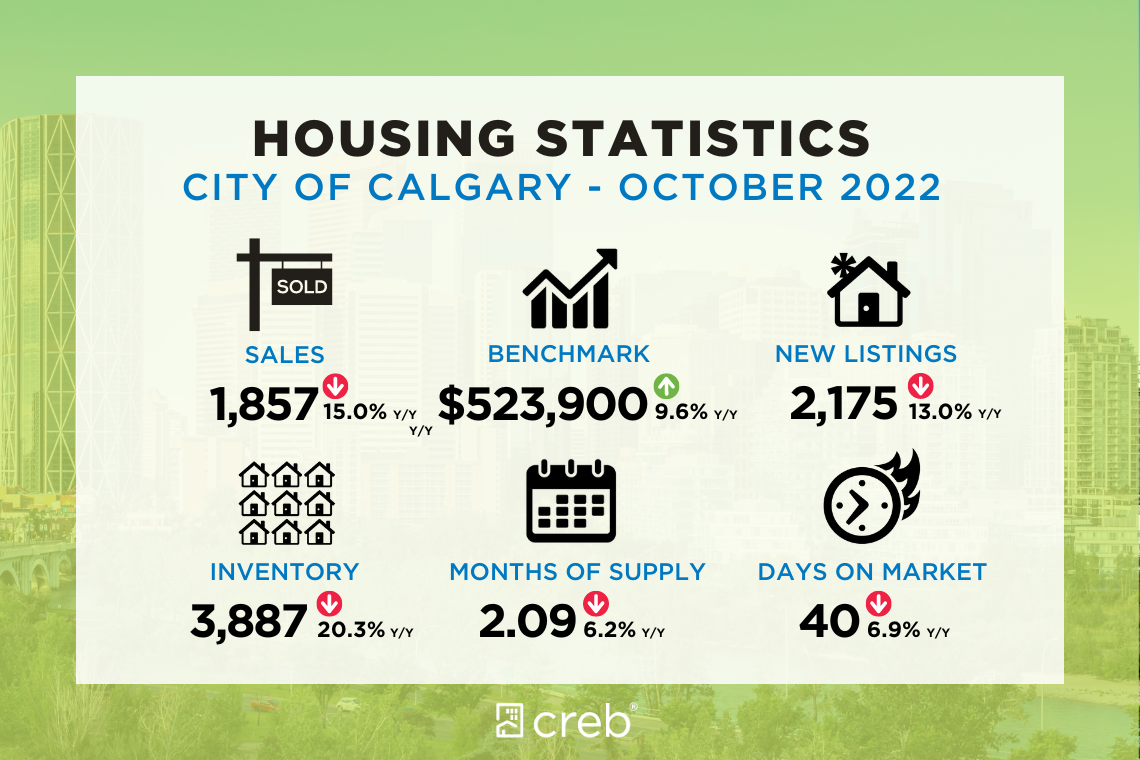

City of Calgary, Nov. 1, 2022 – October sales eased compared to last year’s levels, mostly due to slower activity in the detached sector.

However, with 1,857 sales this month, levels are still stronger than long-term trends and activity reported prior to the pandemic. Year-to-date sales have reached 26,823 and with only two months to go, 2022 will likely post a record year in terms of sales.

“Calgary hasn’t seen the same degree of pullback in housing sales like other parts of Canada, thanks to persistently strong demand for our higher density product,” said CREB® Chief Economist Ann-Marie Lurie. “While our city is not immune to the impact that inflation and higher rates are having, strong employment growth, positive migration flows and a stronger commodity market are helping offset some of that impact.”

New listings also trended down this month causing the sales-to-new-listings ratio to rise to 85 per cent and inventories to trend down. Much of the inventory decline has been driven by product priced below $500,000.

While conditions are not a tight as what was seen earlier in the year, with only two months of supply, conditions remain tighter than historical levels. We are also seeing divergent trends in the market with conditions continuing to favour the seller in the lower-price ranges and shifting to more balanced conditions in the upper-price ranges.

As of October, prices have eased by four per cent relative to the highs reached in May. This is considered a relatively small adjustment when considering price movements in other large cities. It is also important to note that the October benchmark price is still nearly 10 per cent higher than levels reported last year.

In October, inventory levels for detached homes were under 2,000 units, nearly 35 per cent lower than typical levels reported for the month. Moreover, over 42 per cent of the inventory falls in the upper-price ranges of the market. This is likely creating a situation where pricing trends will vary depending on price range.

Overall, detached prices did trend down relative to last month and peak levels in May but remain nearly 12 per cent higher than levels reported last October. The strongest year-over-year price gains have occurred in the North and South East districts.

While sales remain lower than last year’s levels in October, recent pullbacks have not offset gains from earlier in the year and year-to-date sales improved by nearly three per cent. A pullback in new listings relative to sales caused the sales-to-new-listings ratio to push above 80 per cent this month and inventories to ease, leaving the months of supply just over two months.

The benchmark price, while easing slightly compared to last month, remained over nine per cent higher than last year’s levels. Year-over-year price gains have varied from a low of nearly eight per cent in the City Centre to a high of 16 per cent in the North district.

Row sales continue to rise relative to last year supporting a year-to-date gain of nearly 42 per cent. At the same time, new listings this month eased ensuring that the sales-to-new-listings ratio remain exceptionally tight at 106 per cent. Falling inventories and improving sales have ensured this market continues to favour the seller with less than two months of supply. This has also prevented the same adjustment in price.

As of October, the benchmark price was $361,200, less than one per cent lower than the peak achieved in June of this year. Overall, prices remained nearly 15 per cent higher than last year’s levels. The strongest price gains occurred in the South East, North East and North districts.

Apartment sales continue to rise over levels reported last year contributing to the year-to-date increase of over 56 per cent. Improving sales were also met with gains in new listings, but as the growth in sales outpaced the new listings activity, inventory levels continue to trend down. As of October, the months of supply remained just below three months, the lowest level recorded in October since 2013.

In October, the benchmark price was $277,800, similar to last month and nearly 11 per cent higher than last year’s levels. Some of the strongest price gains have occurred in areas outside of the City Centre. Despite persistent price growth, overall prices remain nine per cent below previous highs set back in 2014.

Easing sales over the past several months have not been enough to offset earlier gains as year-to-date sales reached 2,269 units, over 11 per cent higher than last year and on pace to hit a new record high. The growth in sales was possible thanks to a boost in new listings this year. However, the gains in new listings did little to impact inventory levels which remained well below levels traditionally seen in the market in October.

While conditions are not as tight as they were earlier in the year, the months of supply remained exceptionally tight at one and a half months. Despite persistently tight conditions, prices have trended lower from the earlier highs. Airdrie hit a record high price back in April of this year at $510,700, prices have since fallen by six per cent since then yet remain over 14 per cent higher than levels reported last year.

A pullback in new listings relative to sales activity caused the sales-to-new-listings ratio to push up to 90 per cent once again, causing inventories to trend down relative to last month. While overall inventories still remain higher than the exceptionally low levels seen last year, levels are still well below what is typically seen in the market.

While prices have eased off recent highs, at a benchmark price of $507,000, prices remain over 16 per cent higher than last years levels. Price growth has been mostly driven by the detached and semi-detached sector which have reported year-over-year gains exceeding 18 per cent.

A pullback in new listings likely weighed on sales this month as the sales-to-new-listings ratio pushed above 100 per cent causing inventories to remain exceptionally low for October. While conditions are still not as tight as they were earlier in the year, the shift this month did little to support more balanced conditions.

Persistently tight conditions did slow the pace of adjustment in prices as the benchmark price was $537,800 in October. While prices have eased from the high reported in May, they remain over 11 per cent higher than last years levels.

However, with 1,857 sales this month, levels are still stronger than long-term trends and activity reported prior to the pandemic. Year-to-date sales have reached 26,823 and with only two months to go, 2022 will likely post a record year in terms of sales.

“Calgary hasn’t seen the same degree of pullback in housing sales like other parts of Canada, thanks to persistently strong demand for our higher density product,” said CREB® Chief Economist Ann-Marie Lurie. “While our city is not immune to the impact that inflation and higher rates are having, strong employment growth, positive migration flows and a stronger commodity market are helping offset some of that impact.”

New listings also trended down this month causing the sales-to-new-listings ratio to rise to 85 per cent and inventories to trend down. Much of the inventory decline has been driven by product priced below $500,000.

While conditions are not a tight as what was seen earlier in the year, with only two months of supply, conditions remain tighter than historical levels. We are also seeing divergent trends in the market with conditions continuing to favour the seller in the lower-price ranges and shifting to more balanced conditions in the upper-price ranges.

As of October, prices have eased by four per cent relative to the highs reached in May. This is considered a relatively small adjustment when considering price movements in other large cities. It is also important to note that the October benchmark price is still nearly 10 per cent higher than levels reported last year.

Detached

Sales growth in the over $700,000 price range this month were not enough to offset the declines in the lower-price ranges, causing detached sales to ease by over 29 per cent compared to last year. Limited supply growth in the lower-price ranges continue to keep conditions exceptionally tight for lower-priced detached homes.In October, inventory levels for detached homes were under 2,000 units, nearly 35 per cent lower than typical levels reported for the month. Moreover, over 42 per cent of the inventory falls in the upper-price ranges of the market. This is likely creating a situation where pricing trends will vary depending on price range.

Overall, detached prices did trend down relative to last month and peak levels in May but remain nearly 12 per cent higher than levels reported last October. The strongest year-over-year price gains have occurred in the North and South East districts.

Semi-Detached

While sales remain lower than last year’s levels in October, recent pullbacks have not offset gains from earlier in the year and year-to-date sales improved by nearly three per cent. A pullback in new listings relative to sales caused the sales-to-new-listings ratio to push above 80 per cent this month and inventories to ease, leaving the months of supply just over two months.The benchmark price, while easing slightly compared to last month, remained over nine per cent higher than last year’s levels. Year-over-year price gains have varied from a low of nearly eight per cent in the City Centre to a high of 16 per cent in the North district.

Row

Row sales continue to rise relative to last year supporting a year-to-date gain of nearly 42 per cent. At the same time, new listings this month eased ensuring that the sales-to-new-listings ratio remain exceptionally tight at 106 per cent. Falling inventories and improving sales have ensured this market continues to favour the seller with less than two months of supply. This has also prevented the same adjustment in price.As of October, the benchmark price was $361,200, less than one per cent lower than the peak achieved in June of this year. Overall, prices remained nearly 15 per cent higher than last year’s levels. The strongest price gains occurred in the South East, North East and North districts.

Apartment Condominium

Apartment sales continue to rise over levels reported last year contributing to the year-to-date increase of over 56 per cent. Improving sales were also met with gains in new listings, but as the growth in sales outpaced the new listings activity, inventory levels continue to trend down. As of October, the months of supply remained just below three months, the lowest level recorded in October since 2013.In October, the benchmark price was $277,800, similar to last month and nearly 11 per cent higher than last year’s levels. Some of the strongest price gains have occurred in areas outside of the City Centre. Despite persistent price growth, overall prices remain nine per cent below previous highs set back in 2014.

REGIONAL MARKET FACTS

Airdrie

Easing sales over the past several months have not been enough to offset earlier gains as year-to-date sales reached 2,269 units, over 11 per cent higher than last year and on pace to hit a new record high. The growth in sales was possible thanks to a boost in new listings this year. However, the gains in new listings did little to impact inventory levels which remained well below levels traditionally seen in the market in October.While conditions are not as tight as they were earlier in the year, the months of supply remained exceptionally tight at one and a half months. Despite persistently tight conditions, prices have trended lower from the earlier highs. Airdrie hit a record high price back in April of this year at $510,700, prices have since fallen by six per cent since then yet remain over 14 per cent higher than levels reported last year.

Cochrane

A pullback in new listings relative to sales activity caused the sales-to-new-listings ratio to push up to 90 per cent once again, causing inventories to trend down relative to last month. While overall inventories still remain higher than the exceptionally low levels seen last year, levels are still well below what is typically seen in the market.While prices have eased off recent highs, at a benchmark price of $507,000, prices remain over 16 per cent higher than last years levels. Price growth has been mostly driven by the detached and semi-detached sector which have reported year-over-year gains exceeding 18 per cent.

Okotoks

A pullback in new listings likely weighed on sales this month as the sales-to-new-listings ratio pushed above 100 per cent causing inventories to remain exceptionally low for October. While conditions are still not as tight as they were earlier in the year, the shift this month did little to support more balanced conditions.Persistently tight conditions did slow the pace of adjustment in prices as the benchmark price was $537,800 in October. While prices have eased from the high reported in May, they remain over 11 per cent higher than last years levels.

Click here to view the full City of Calgary monthly stats package.